Execution Debt

Why Busy Companies Stop Compounding

Most companies do not stall because of one catastrophic decision. They stall because of all the decisions the founder never completes. The calendar stays full. The team stays busy. The meetings keep happening. Still, the company does not compound.

This is execution debt: the compound interest on unfinished leadership.

Execution debt is the drag that accumulates when unresolved decisions, recurring frictions, untaught standards, and unprotected time become normal operating procedures.

The Four Doors of Execution Debt

In founder-led companies, execution debt usually enters through four doors:

1. Unmade decisions teach the company to wait.

2. Unowned frictions turn internal mess into customer-facing failure.

3. Untaught standards trap quality inside the founder’s head.

4. Unprotected time lets urgency steal the company’s future.

Once these four forces become normal, the company can look active from the outside while quietly losing the internal capacity to compound.

Activity is motion / Execution is closure

That is why a founder can work sixty hours, run twelve meetings, answer every message, and still end the week in the same place.

The pattern becomes visible on Monday morning. The founder opens the inbox before opening the calendar. A customer issue hijacks the first hour. A team question exposes last week’s unfinished decision. A meeting is added because no one owns the answer. By noon, the founder has been busy for four hours and has closed nothing. The weak have inherited the debt.

The enemy is not lack of effort. The enemy is unresolved work masquerading as progress.

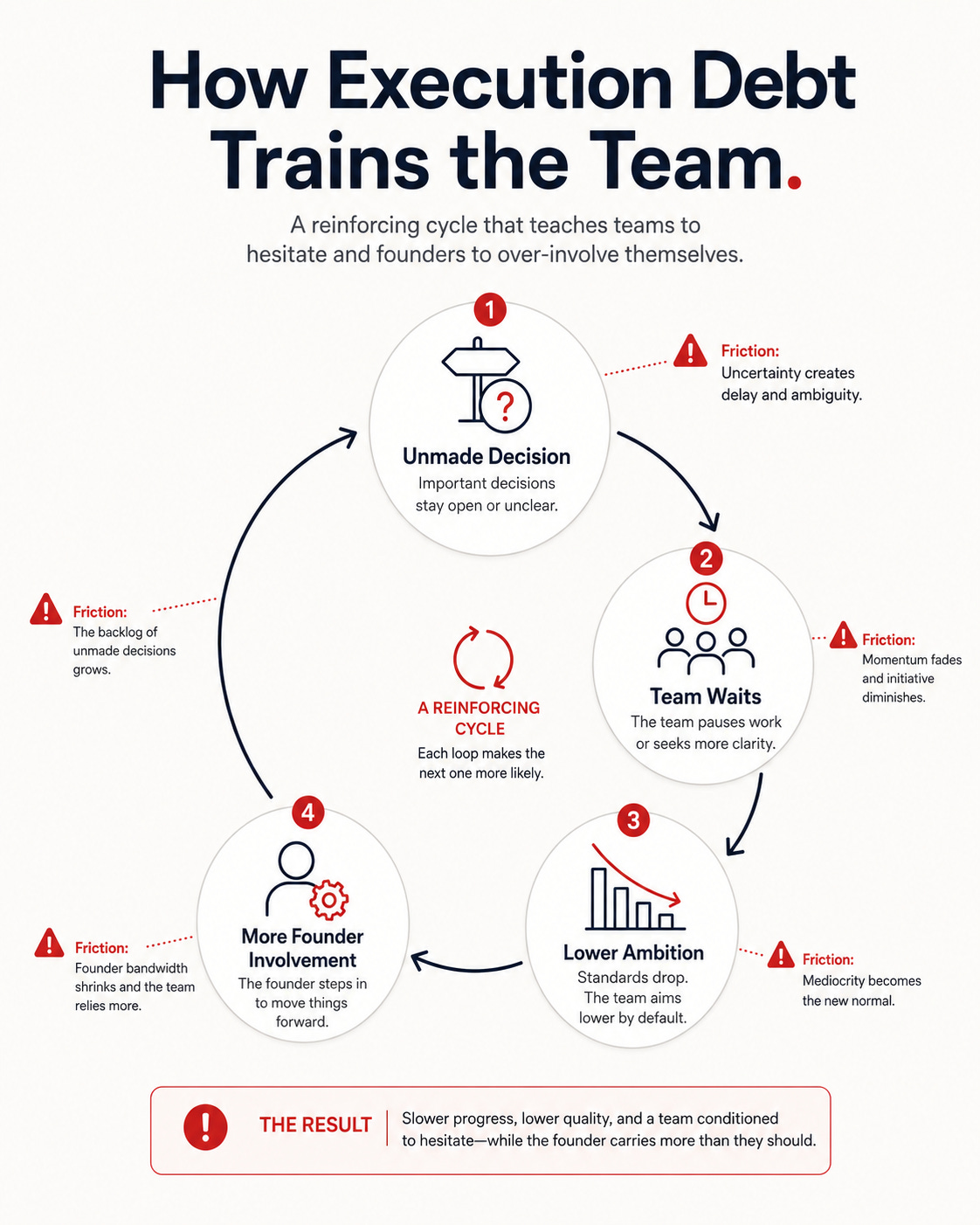

How Execution Debt Trains the Team

A pricing exception that should have been settled three weeks earlier consumes forty minutes in a leadership meeting. The sales lead stops pushing because they no longer know what is allowed. The customer goes cold because the company looks uncertain. Finance builds three versions of a model nobody trusts. The founder calls it collaboration. It is an organizational interest expense.

The same pattern appears in operations. A billing discrepancy is deferred because no one owns the solution Support invents workarounds. Customers lose trust. Credits appear. Churn rises. Sales has to replace revenue the company should never have lost. A process gap becomes revenue drag.

Execution debt also grows when leaders make decisions but refuse to let them stay made. They revisit the pricing model after every objection. They rewrite the strategy after every slow month. They change priorities every time a new opportunity appears. Reopened decisions punish the people who already started executing. Over time, the safest move is to wait.

The team eventually learns that no decision is real until the founder stops considering it. At that point, people do not execute decisions. They wait for moods, signals, reversals, and exceptions.

Eventually, talented people adapt downward. They stop pushing because the decision may change. They stop solving because ownership is unclear. They stop bringing judgment because preference keeps replacing it. Execution debt trains the team to lower its ambition.

Culture is not what the founder announces. It is what the organization learns it can repeatedly leave unfinished. Meetings without decisions, customer issues without owners, and standards trapped inside the founder’s head become the real culture.

The Founder Dependency Trap

Founder dependency often disguises itself as quality control when founders mistake taste for standards.

Taste can live in the founder’s head. A standard has to be taught, inspected, documented, and repeated. Until that happens, the team is meeting the standard. They are guessing at an invisible one. If the founder cannot explain the standard, the team cannot be accountable to it.

In investor language, this is key-person risk. In operator language, this is called execution debt. Either way, the company has not yet separated performance from the founder’s constant intervention.

Key Person Risk & How to Manage It

Execution debt lowers the value of the company because it turns the founder into infrastructure instead of leadership. If decisions, standards, quality control, and escalation all run through one person, the business may have revenue, but it does not yet have transferable enterprise value.

This does not mean leaders should be reckless. It means they should stop mistaking delay for diligence. Gather what is knowable, name the remaining risks, make the call, and let reality teach the organization.

Often, almost deciding is more expensive than deciding wrong. A wrong decision produces information. An almost-decision produces waiting. The danger is not that every decision will be correct. The danger is that unresolved decisions prevent the company from learning anything at all.

Founder Dependency: The Hidden Ceiling on Your Company’s Growth | Gene Hammett

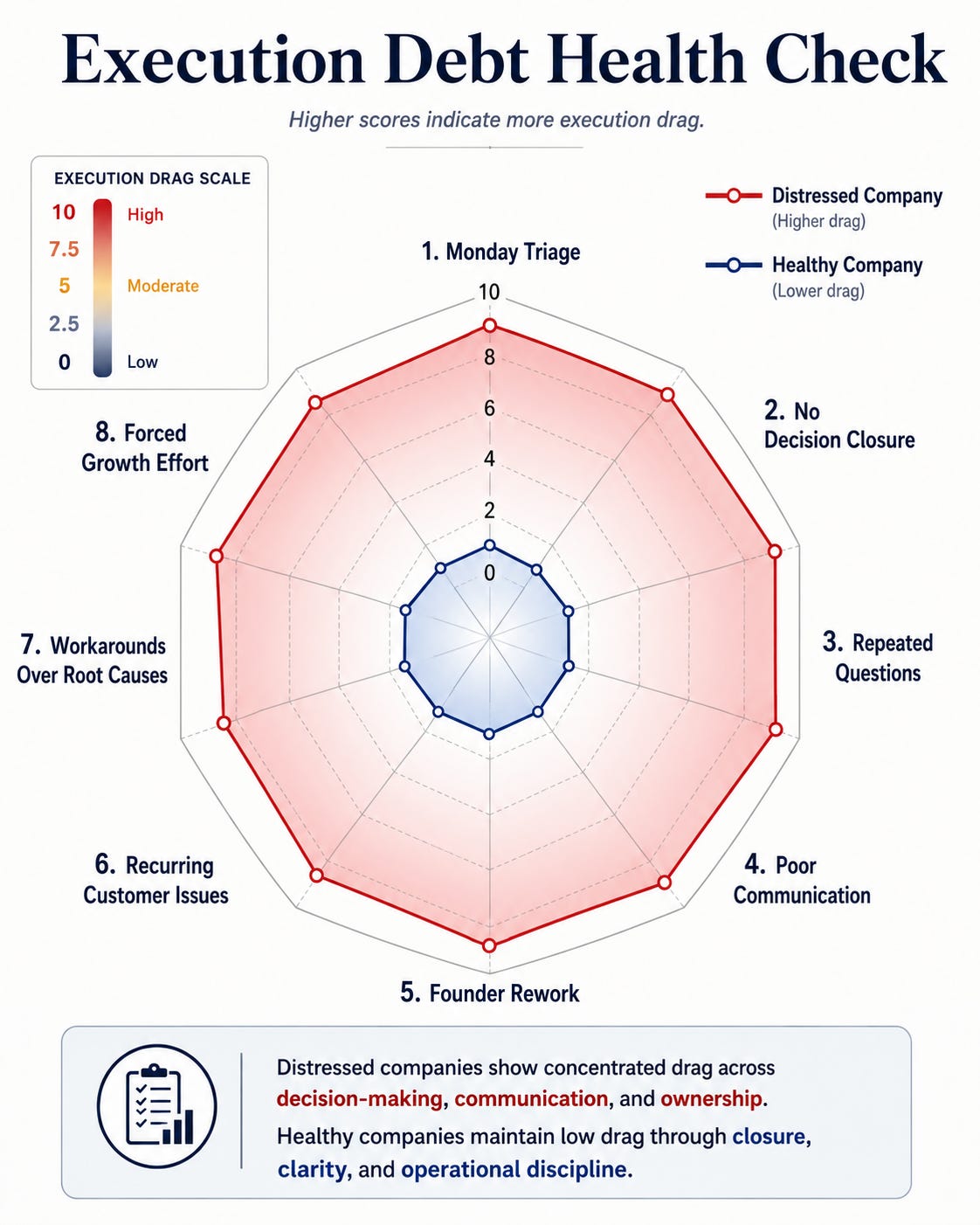

How to Find Execution Debt

The easiest way to find execution debt is to look for recurring confusion. Wherever the same question, complaint, delay, exception, or workaround continues to return, the company is paying interest on something leadership has not closed.

Execution debt is accumulating if:

Monday begins with triage instead of execution.

Meetings end without decisions.

The team keeps asking the same questions.

Decisions are made privately but never clearly communicated.

The founder keeps taking work back.

Customer issues keep recurring.

People create workarounds instead of fixing root causes.

Growth requires more force every month.

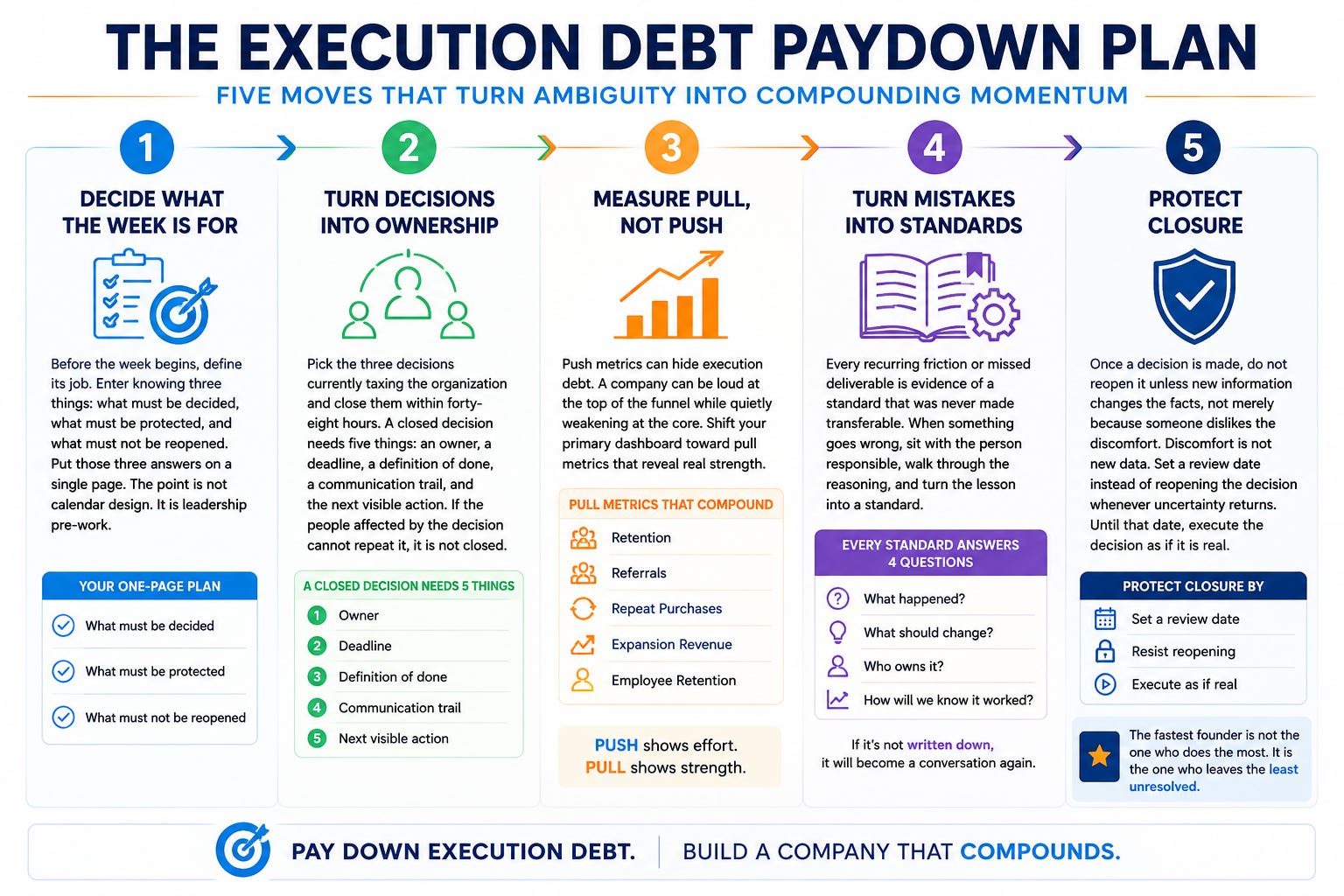

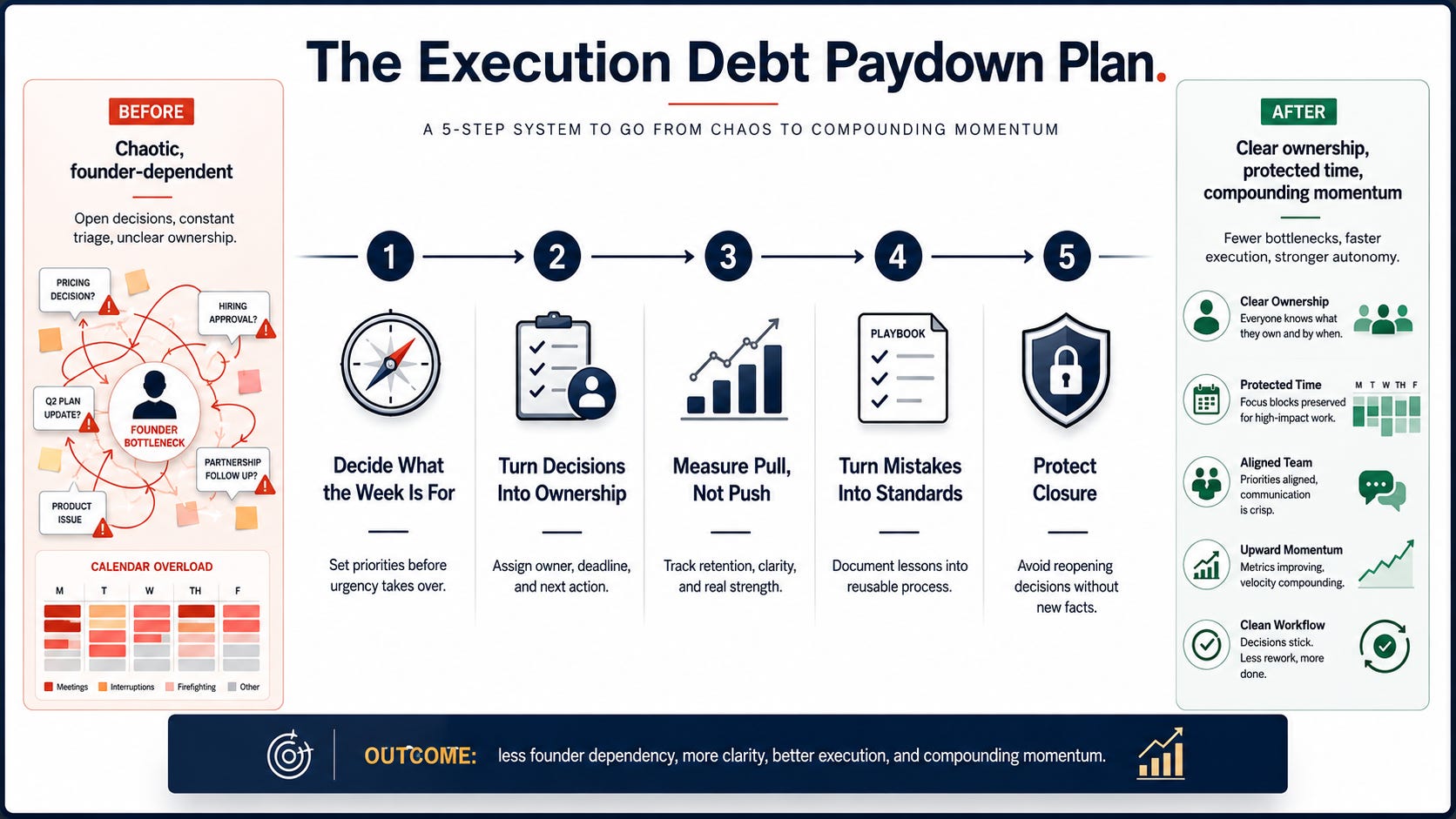

The Execution Debt Paydown Plan

Alex Hormozi’s Biggest Lie | Key Man Dependency | Justin Brock

You do not eliminate execution debt with a productivity hack. You pay it down by turning ambiguity into decisions, decisions into ownership, and ownership into standards. The goal is not to make the founder busier. It is to make fewer things depend on the founder at all

.

1. Decide What the Week Is For

Before the week begins, define its job. Enter knowing three things: what must be decided, what must be protected, and what must not be reopened. Put those three answers on a single page. The point is not calendar design. It is leadership pre-work.

2. Turn Decisions Into Ownership

Pick the three decisions currently taxing the organization and close them within forty-eight hours. A closed decision needs five things: an owner, a deadline, a definition of done, a communication trail, and the next visible action. If the people affected by the decision cannot repeat it, it is not closed.

3. Measure Pull, Not Push

Push metrics can hide execution debt. A company can be loud at the top of the funnel while quietly weakening at the core. Shift your primary dashboard toward retention, referrals, repeat purchases, expansion revenue, and employee retention. Employee retention matters because the team is also voting on whether the operating system works. Push tells you how hard the company is trying. Pull tells you whether the business is actually strengthening.

4. Turn Mistakes Into Standards

Every recurring friction or missed deliverable is evidence of a standard that was never made transferable. When something goes wrong, sit with the person responsible, walk through the reasoning, and turn the lesson into a standard. It should answer four questions: What happened? What should change? Who owns it? How will we know it worked? If it is not written down, it will become a conversation again.

5. Protect Closure

Once a decision is made, do not reopen it unless new information changes the facts, not merely because someone dislikes the discomfort. Discomfort is not new data. Set a review date instead of reopening the decision whenever uncertainty returns. Until that date, execute the decision as if it is real. The fastest founder is not the one who does the most. It is the one who leaves the least unresolved.

Most founders are not short on effort. They are short on closure. Eventually, the company becomes a record of every decision leadership was willing — or unwilling — to finish.

Start with one decision that has been open too long. Close it today. That is how busy companies start compounding again.