The AI Capital Strain

Circular Flows, Patchy Returns, and the Reset Operators Must Navigate

Circular capital flows, uneven production returns, and increasingly capable open-weight models are forcing a reset in how we judge artificial-intelligence investments.

Operators who treat generalized model capability as an increasingly substitutable input—and concentrate capital on proprietary data, trusted workflows, distribution, and measurable outcomes—will be better positioned than those continuing to extrapolate the economics of the first hyperscale investment wave.

The next phase of AI will not be judged by how many models are launched, how many pilots are announced, or how much infrastructure is ordered.

It will be judged by whether the systems built around those models generate durable economic value after the complete cost of deployment is counted.

That accounting must include more than inference charges. It must include data preparation, integration, human review, correction, security, compliance, process redesign, exception handling, maintenance, and the cost of being dependent on a provider whose prices, policies, or availability may change.

The central question is no longer whether artificial intelligence is useful.

It is whether the capital committed to generalized AI infrastructure can produce returns proportionate to its extraordinary cost—and whether individual operators are building businesses that remain defensible as model capabilities become less scarce.

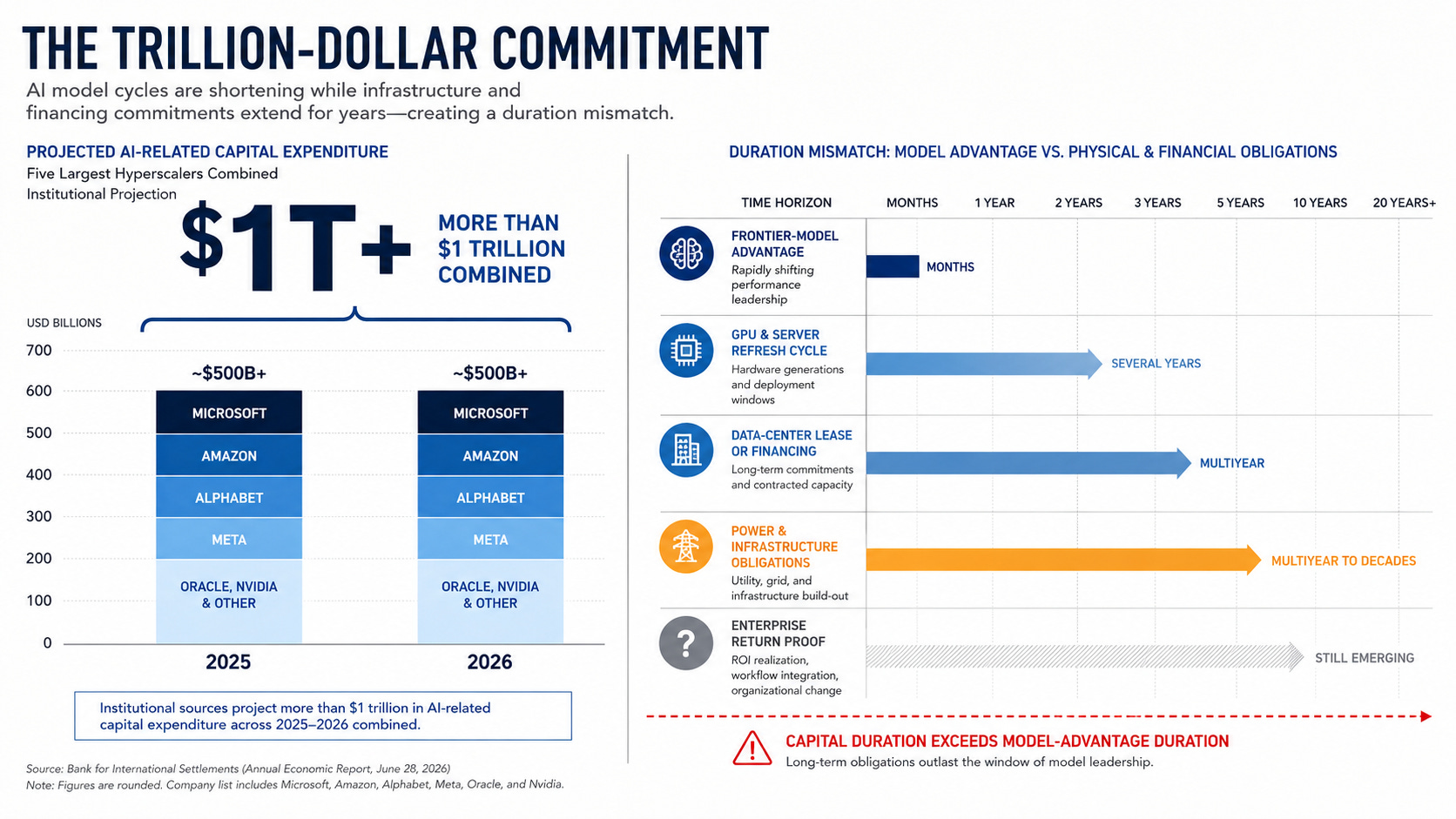

The Scale of the Capital Bet

The risk is no longer theoretical.

In its 2026 Annual Economic Report, the Bank for International Settlements estimated that the five largest hyperscalers would spend more than $1 trillion on AI-related capital expenditure across 2025 and 2026.

The BIS did not argue that artificial intelligence lacks economic value. It warned that an investment boom built on exceptionally high expectations becomes vulnerable when infrastructure spending expands faster than demonstrated returns.

At some companies, the scale of AI investment is beginning to exceed internally generated cash flow, increasing the importance of debt, structured finance, infrastructure partnerships, and outside capital.

That distinction matters.

Technology companies are not merely purchasing more software. They are constructing enormous physical systems involving land, electricity, water, cooling, semiconductors, networking equipment, substations, transmission infrastructure, data centers, long-duration contracts, and specialized labor.

The financial commitment therefore extends well beyond the useful life of any individual model generation.

A model can lose its performance advantage within months. A data center, power contract, or structured credit facility may remain on the books for years.

The largest technology companies have experienced an extraordinary expansion in market value, becoming a major source of support for U.S. equity markets and economic sentiment.

Their balance sheets remain formidable. But the relationships connecting model developers, cloud providers, chipmakers, infrastructure companies, and financial sponsors make it increasingly difficult to isolate independent end-customer demand.

One arrangement illustrates the issue.

Google has made substantial investments in Anthropic. Anthropic, meanwhile, reportedly committed to purchasing approximately $200 billion in Google Cloud infrastructure and chips over five years.

The arrangement may be commercially rational for both parties. Anthropic secures access to enormous amounts of compute, while Google strengthens utilization and future demand for its cloud platform.

But the structure also creates a circular economic relationship: the infrastructure provider finances a model company that then becomes one of the infrastructure provider’s largest customers.

This arrangement does not make the revenue fictitious.

It makes its interpretation more complicated.

AI’s circular spending problem? Activate CEO Michael Wolf on the circular AI economy

Similar relationships exist throughout the AI ecosystem.

Cloud credits, strategic investments, chip-financing arrangements, capacity guarantees, equity stakes, and long-term purchase commitments can support rapid reported growth while making it harder to determine how much demand originates from unrelated enterprises generating durable returns of their own.

The circularity is not necessarily evidence of wrongdoing. Industrial ecosystems often develop through strategic investments, supplier financing, customer commitments, and long-term partnerships.

The concern is concentration.

If the same limited group of companies funds, supplies, purchases from, and assigns valuations to one another, headline growth may reveal less about independent market adoption than investors initially assume.

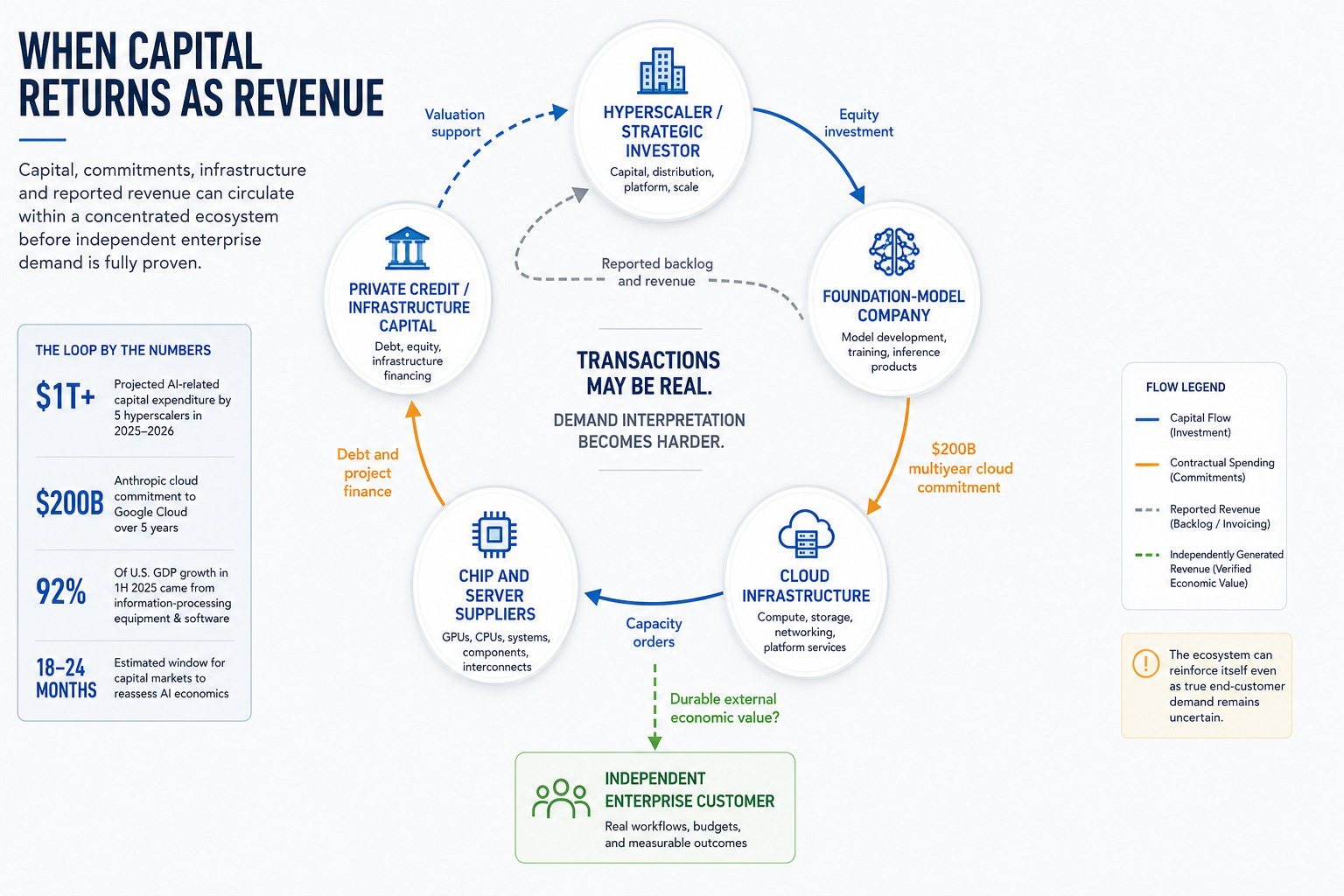

The Capital Loop

The modern AI economy can involve several interconnected steps.

An investor or hyperscaler provides capital to a model developer.

The model developer commits a substantial share of that capital to cloud infrastructure.

The cloud provider uses the demand commitment to justify additional data-center capacity and semiconductor purchases.

The chip supplier reports increased sales and may reinvest in adjacent model, cloud, or infrastructure companies.

Those companies then use the newly raised capital to purchase more compute.

Every transaction may be contractually valid. Every participant may be acting rationally.

But the system can still amplify the appearance of demand before the final customer has demonstrated a comparable amount of independent economic value.

That leaves the central operating question unresolved:

How much independent economic value is being created for the organizations that ultimately pay for AI-enabled products and services?

This does not dismiss AI’s demonstrated utility.

Recommendation systems transformed advertising, commerce, entertainment, and logistics long before the current generative-AI cycle.

Coding assistants can accelerate some development tasks.

Models are delivering real value in document processing, fraud detection, customer support, scientific research, translation, search, and narrowly defined analytical workflows.

The greatest pressure is concentrated elsewhere: generalized foundation-model infrastructure and broad enterprise mandates funded before their full operating costs were understood.

Where Returns Become Harder to Measure

Benchmark performance does not automatically translate into production economics.

Once models enter real workflows, organizations must account for data preparation, integration, evaluation, human review, exception handling, security, compliance, process redesign, and ongoing monitoring.

These costs are frequently treated as temporary implementation friction.

In many environments, they are a permanent part of the operating model.

That distinction determines whether AI creates genuine productivity or merely relocates labor.

A system that produces a draft in seconds may appear highly efficient. If employees must then verify every factual claim, correct formatting, restore missing context, resolve edge cases, and accept responsibility for the final result, the relevant metric is not generation speed.

It refers to the cost and quality of the entire production cycle.

The AI Investment Boom: When Will It Pay Off?

The operational equation should be written plainly:

Net AI value = output value minus generation, review, correction, integration, risk, and maintenance costs.

Many internal business cases measure only the first half of that equation.

They count the time saved during initial generation while ignoring the work required after the output appears.

They compare model speed with manual production but fail to compare the complete AI-assisted process with the complete prior process.

They count a lower headcount in one function but fail to measure higher oversight, engineering, security, or compliance costs elsewhere.

They measure pilot accuracy under controlled conditions but not exception rates at production scale.

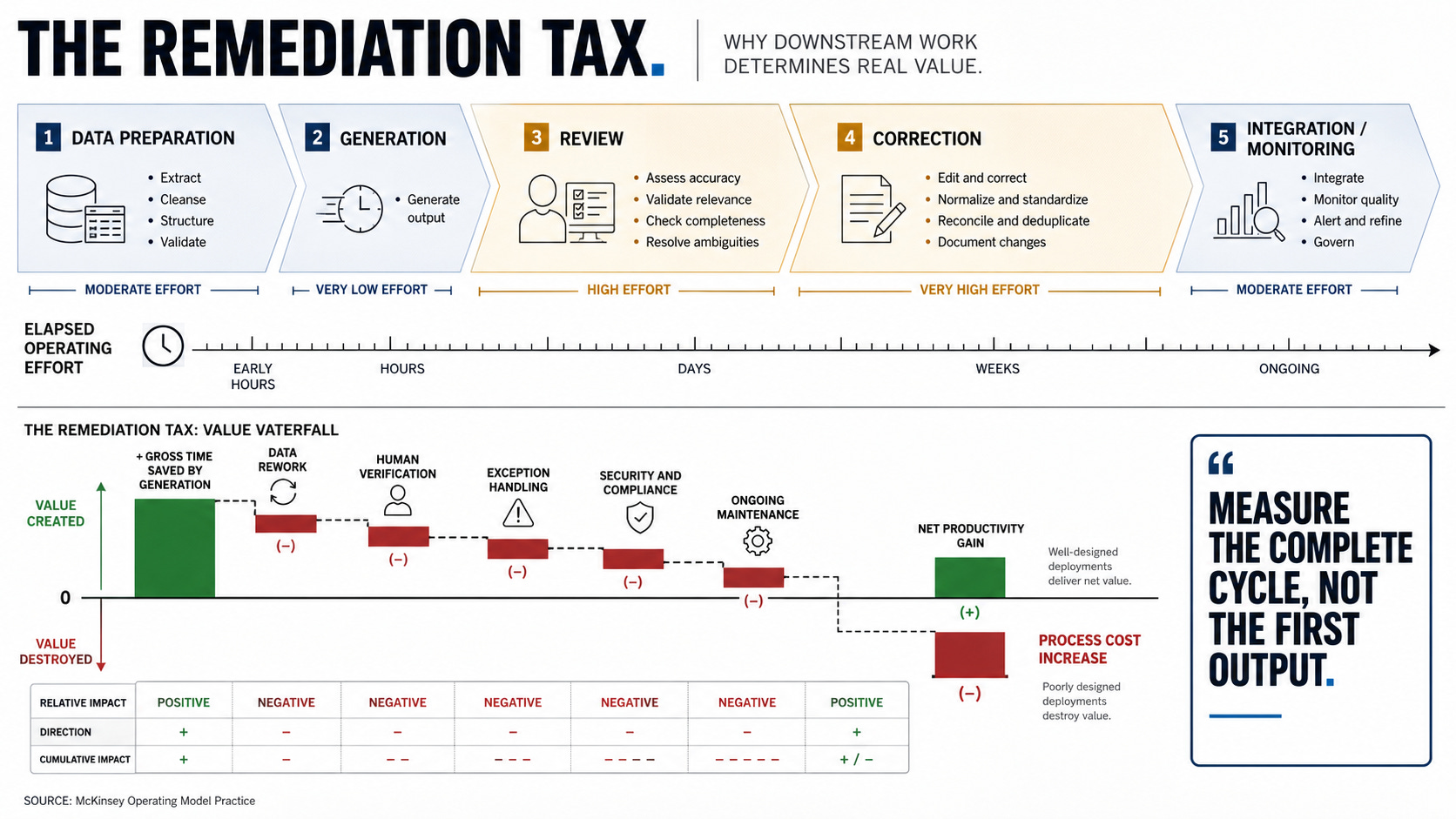

The Remediation Tax

The hidden cost of enterprise AI is often the remediation tax: the human and technical effort required to turn a plausible model output into something reliable enough to use.

This tax can appear in several forms:

Employees correcting inaccurate or incomplete outputs

Engineers building validation and fallback systems

Security teams testing new attack surfaces

Legal teams reviewing privacy and liability exposure

Product teams redesigning interfaces around model uncertainty

Managers handling exceptions and customer complaints

Data teams cleaning or restructuring internal information

Senior experts verifying work that junior systems generated

The Starbucks inventory program offers a concrete example.

Starbucks introduced an automated computer-vision system intended to count items such as milk and syrup inventory across North American stores.

Approximately nine months later, in May 2026, the company discontinued the program after recurring inaccuracies and employee complaints.

The system worked despite computer vision having no value.

It failed because its performance under real store conditions did not reliably improve the complete operating process. Inaccurate counts created additional checks and manual work, weakening the expected labor savings.

Duolingo presents a more complicated case.

The company used AI to increase the speed and volume of course-content production dramatically. It also encountered criticism from users concerned about lesson quality, translation accuracy, and the replacement of human contributors.

Duolingo’s experience is not a simple story of failure. The company has continued to grow and use AI extensively.

Its experience demonstrates that production volume and customer value are different measurements.

AI can allow a company to create far more material, but it still requires human judgment to ensure that the material improves the outcomes that customers actually care about.

The same tension appears in software development.

AI coding tools can increase the volume of generated code, but that volume is not equivalent to maintainable software.

Organizations must still validate architecture, test behavior, secure dependencies, correct vulnerabilities, manage technical debt, and ensure that they can upgrade systems over time.

The scarce resource therefore shifts.

As generation becomes easier, verification, systems judgment, and accountability become more valuable.

The Open-Weight Price Reset

The cost structure is changing at the same time.

Open-weight models developed in the United States, China, Europe, and elsewhere have narrowed the performance gap on many practical workloads.

Models from families such as DeepSeek and Qwen can be downloaded, adapted, and operated on private infrastructure, subject to their individual licenses and hardware requirements.

For many organizations, the appeal extends beyond token pricing.

Locally deployed models give you more control over sensitive information, reduce reliance on a single API provider, allow for specialized fine-tuning, and let applications run in controlled environments without sending every request through an external service.

They are not automatically cheaper in every circumstance.

Local deployment introduces hardware, energy, staffing, optimization, security, and maintenance costs. Proprietary APIs may still be more cost-effective for low-volume usage, rapidly changing frontier capabilities, or workloads that need the strongest available model.

But the strategic direction is becoming clearer.

Organizations increasingly have credible alternatives.

What Is AI Distillation — And How DeepSeek Used It To Blindside OpenAI

Organizations can route unusually complex or high-value tasks to frontier systems while assigning routine classification, extraction, summarization, coding, and internal analysis to less expensive models.

They can switch providers, host selected systems privately, and use multiple models inside the same workflow.

As those options expand, generalized model access becomes more substitutable.

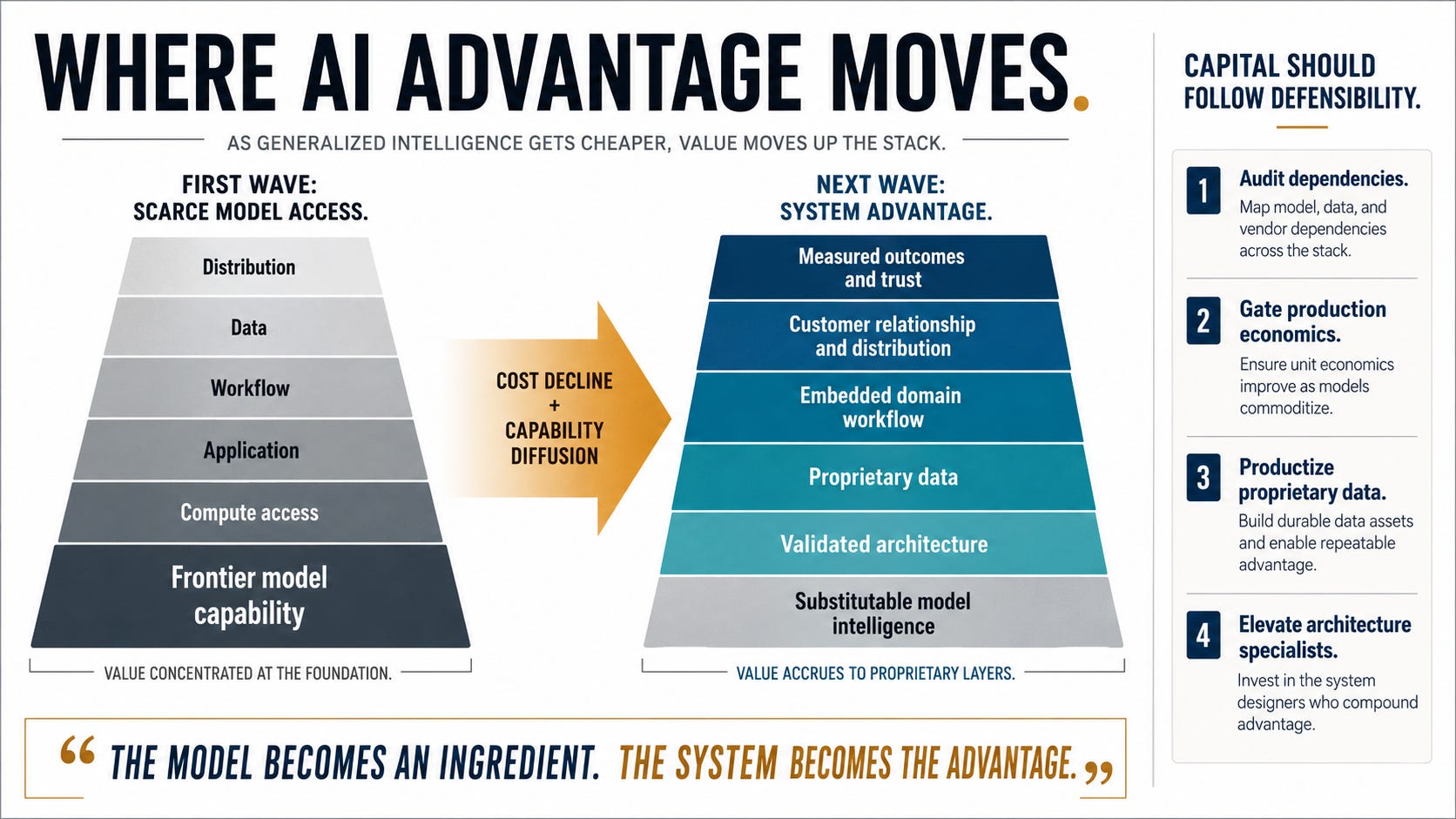

The competitive advantage moves upward into the application and operating layers:

Proprietary and permissioned data

Customer relationships and distribution

Domain-specific evaluation systems

Regulatory knowledge and approval

Embedded workflows

Trusted interfaces

Organizational execution

Feedback systems

The ability to measure and improve real outcomes

The model remains important.

It becomes one component of a larger system rather than the entire strategy.

Where Defensibility Moves

Raw model access is unlikely to disappear as a source of value, particularly at the frontier.

A sustained performance advantage may matter in scientific research, advanced coding, defense, high-value reasoning, autonomous systems, or other domains where marginal capability produces disproportionate returns.

But most enterprises do not compete by training frontier models.

They compete by applying available intelligence to specific customers, decisions, assets, regulations, and workflows.

As baseline capabilities converge, advantage migrates toward the parts of the system competitors cannot acquire through the same API.

A competitor may be able to license the same model.

It should not be able to reproduce the accumulated context, operating knowledge, permissions, integrations, evaluation systems, customer trust, and feedback loops that make the model valuable inside your organization.

The defensible asset is not simply the dataset stored in a warehouse.

It is the functioning system that continually improves that data, applies it inside a valuable workflow, observes outcomes, captures corrections, and converts those corrections into better future decisions.

A Concentrated Economic Expansion

Macroeconomic indicators show how much of the current expansion depends on technology investment.

Harvard economist Jason Furman calculated that investment in information-processing equipment and software represented approximately 4 percent of U.S. GDP but accounted for roughly 92 percent of real GDP growth during the first half of 2025.

The statistic should not be interpreted as evidence that 92 percent of economic growth came directly from generative AI. The underlying category is broader.

It does, however, reveal an unusually concentrated source of incremental growth.

When a relatively small investment category produces such a large share of measured expansion, headline economic strength can conceal weakness elsewhere.

The economy becomes more sensitive to any moderation in data-center construction, semiconductor purchases, software investment, or related infrastructure spending.

Financing structures add another layer.

AI infrastructure increasingly relies on technology-company cash flows as well as private credit, insurers, infrastructure funds, banks, and institutional investors.

These sources can provide long-duration capital for assets that public markets or corporate balance sheets might not finance alone.

They can also distribute risk through structures that are difficult for outside observers to evaluate.

That does not mean the projects will fail.

It means the consequences of lower utilization, weaker pricing, technological obsolescence, construction delays, or declining model costs may extend beyond the companies making the initial announcements.

The infrastructure may remain productive while earning lower returns than its financing originally assumed.

That is the central distinction between technological success and investment success.

AI can transform the economy while some of the capital deployed during the transformation still earns disappointing returns.

Four Priorities for Capital Discipline

Operators cannot control hyperscaler spending or predict when financial markets will reassess the sector.

They can reduce their exposure to the most durable assumptions.

1. Audit Every External Model Dependency

Map every workflow that depends on a closed model or external API.

Measure current usage, projected volume, switching costs, data restrictions, latency requirements, failure modes, and the financial effect of different pricing scenarios.

Then test alternatives under realistic operating conditions.

Some workloads will continue to justify frontier proprietary models.

Others may perform adequately with smaller proprietary systems, open-weight models, conventional software, deterministic rules, or hybrid architectures.

The objective is not to eliminate external providers.

This is to prevent a replaceable model dependency from becoming an uncontrolled strategic concentration.

The audit should answer five questions:

What happens if the provider doubles its price?

What happens if the provider changes its usage policy?

What happens if the model becomes unavailable in a critical geography?

How long would migration take?

Does a lower-cost alternative produce an acceptable result after the full review cycle is counted?

2. Establish Production Gates Before Scaling

Do not evaluate AI initiatives solely on model accuracy, benchmark scores, demonstration quality, or the speed of first-generation output.

Require teams to measure the complete workflow:

Data preparation

Generation

Review

Correction

Escalation

Integration

Monitoring

Compliance

Maintenance

An initiative should scale only when the full system reduces total human effort, improves net quality, increases revenue, lowers risk, or delivers another explicitly defined operating benefit.

Remediation work should be treated as a primary metric rather than hidden inside implementation budgets.

Projects that fail this test should be redesigned, narrowed, or stopped.

They should not be defended indefinitely on the assumption that the next model release will repair an uneconomic process.

Every production gate should include a baseline comparison with the prior workflow.

Without that baseline, an organization may know that the model performs impressively while remaining unable to demonstrate that the business performs better.

3. Stop Treating Model Access as the Entire Strategic Asset

Generalized intelligence is becoming cheaper and more widely available.

That does not make models irrelevant.

It reduces the durability of strategies based only on access to them.

Capital should increasingly move toward assets that improve with organizational use:

Clean internal datasets

Verified institutional knowledge

Customer interaction histories

Workflow integrations

Specialized evaluation environments

Regulatory permissions

Distribution channels

Feedback systems

Trusted brands and relationships

These assets require less glamorous work than announcing a new foundation-model partnership.

They require data governance, labeling, permissions, process mapping, integration, evaluation, and continuous maintenance.

They are also more difficult for competitors to reproduce.

4. Elevate the Architecture Specialists

As routine generation improves, organizations will need fewer people whose primary advantage is producing undifferentiated volume.

They will need more people who can design, evaluate, secure, integrate, and maintain complex systems.

Senior technical talent should focus on the following:

Systems architecture

Model and vendor selection

Evaluation design

Security hardening

Data governance

Failure analysis

Human-control mechanisms

Upgrade planning

Cost and performance optimization

Provider portability

Long-term maintainability

Compensation and promotion systems should reflect this change.

The most valuable operators may not be those who generate the most code or launch the most pilots.

They may be those who prevent fragile systems from reaching production, identify hidden costs before they compound, and construct architectures capable of surviving changes in models, vendors, prices, regulation, and organizational priorities.

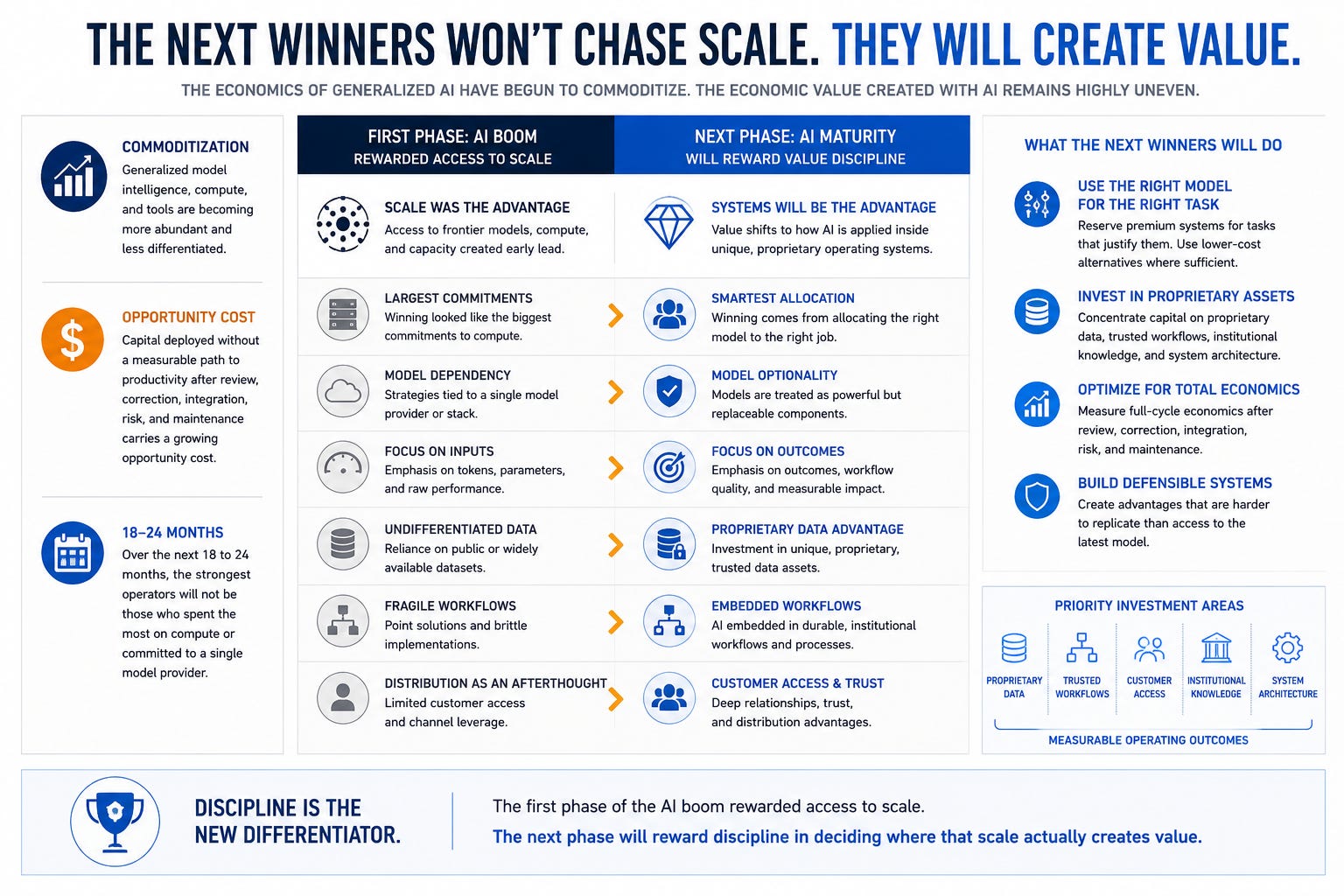

The Reset

The economics of generalized AI have begun to commoditize, but the economic value created with AI remains highly uneven.

Capital deployed without a measurable path to productivity after review, correction, integration, risk, and maintenance carries a growing opportunity cost.

Over the next 18 to 24 months, the strongest operators are unlikely to be those that made the largest undifferentiated commitments to compute or tied their strategies to a single model provider.

They will be the organizations that treated models as powerful but replaceable components.

They will reserve premium systems for tasks that justify them, use lower-cost alternatives where they are sufficient, and concentrate investment on proprietary data, trusted workflows, customer access, institutional knowledge, system architecture, and measurable operating outcomes.

The first phase of the AI boom rewarded access to scale.

The next phase will reward discipline in deciding where that scale actually creates value.