The Blueprint for Building a Business That Lasts

Strategies, Statistics, and Success Stories for Today's Ambitious Entrepreneurs

Why This Matters Now - The startup landscape has never been more accessible or more ruthless. With 150 million startups worldwide competing for attention and 90% destined to fail, the entrepreneurs who win are those who master the fundamentals while thinking differently. This is your roadmap to becoming part of the 10% who don’t just survive but build empires.

The Brutal Truth About Startup Success

Let’s get real about the numbers. The global startup failure rate stands at 90%. That statistic hasn’t budged significantly since the 1990s, despite revolutionary advances in technology, funding mechanisms, and business intelligence tools. The fundamentals of building a successful company remain as challenging as ever.

But here’s what separates the winners from the rest: knowledge, strategy, and relentless execution.

First-time founders face an 18% success rate. Those who’ve failed before improve slightly to 20%. But entrepreneurs with a successful exit behind them? They hit a 30% success rate. Experience compounds. Learning accelerates. And the principles outlined here will compress your learning curve dramatically.

Principle 1: Start With What You Have, Not What You Think You Need

The myth of the well-funded startup dies hard. We’ve been conditioned to believe that success requires massive capital, but the data tells a different story.

31% of startup capital for employer firms is less than $10,000. The average cost of launching a startup? Just $3,000.

Sara Blakely launched Spanx with $5,000 in personal savings. She didn’t have a business degree, prior fashion industry experience, or investor backing. What she had was a problem she’d personally experienced, a solution she’d prototyped herself, and unwavering belief in her vision. That $5,000 investment built a billion-dollar brand.

Whitney Wolfe Herd founded Bumble after being pushed out of Tinder, transforming workplace adversity into entrepreneurial fuel. She didn’t wait for perfect conditions or unlimited resources. She identified a gap in how women experienced dating apps and moved decisively to fill it.

The lesson is clear: constraints breed creativity. When you’re not drowning in capital, you’re forced to validate every assumption, test every hypothesis, and earn every customer. That discipline becomes your competitive advantage.

Principle 2: The Convergence Model: Where Passion Meets Utility

Great businesses emerge from a specific intersection: what you’re passionate about and what genuinely helps others.

Phil Knight didn’t just love running shoes. He was obsessed with making them better. That obsession drove him to study footwear design, understand athlete biomechanics, and eventually build Nike into a $180 billion brand. His passion created utility for millions of athletes worldwide.

Reshma Saujani founded Girls Who Code after recognizing a critical gap in tech education. Her passion for gender equity combined with practical skill-building has now reached over 500,000 girls globally, proving that mission-driven ventures can scale massively while doing profound good.

Ask yourself these questions:

What problems do I understand deeply because I’ve lived them?

What skills have I developed that others would pay to access?

Where does my enthusiasm intersect with genuine market needs?

The answers reveal your unique opportunity space.

Principle 3: Value Creation Is Everything

Here’s the core truth that separates successful entrepreneurs from struggling ones: value means helping people meet emotional needs.

Customers don’t buy products. They buy better versions of themselves. They buy confidence, status, belonging, peace of mind, and transformation.

Patagonia doesn’t sell outdoor gear. They sell environmental activism and adventure identity. Their “Don’t Buy This Jacket” campaign actually increased sales because it aligned perfectly with their customers’ values around sustainability and conscious consumption.

Tesla doesn’t sell electric vehicles. Elon Musk sells a vision of the future where technology solves humanity’s greatest challenges. Every Tesla owner becomes part of that narrative, and that emotional connection justifies premium pricing.

To create genuine value, answer these questions:

What problem does my offering solve?

What emotional state does my customer want to achieve?

How does my solution make them feel about themselves?

Value isn’t what you build. It’s what your customer experiences.

Watch how this principle powered one entrepreneur’s rapid growth: Y Combinator’s “How to Build a Product that Scales” breaks down the value creation framework that’s launched thousands of successful startups.

Principle 4: The Lean Launch Method

The data is unambiguous: 34% of startups that fail lack proper product-market fit. They build what they assume customers want instead of what customers actually need.

The solution? Start small, test fast, iterate constantly.

This isn’t about being cautious. It’s about being scientific. Every assumption becomes a hypothesis. Every launch becomes an experiment. Every customer interaction generates data that shapes your next move.

Dropbox famously validated demand before building their product by creating a simple explainer video. The video demonstrated how the service would work, and signups exploded overnight. They’d confirmed product-market fit before writing significant code.

The lean launch framework:

Identify your riskiest assumption

Design the smallest possible test to validate it

Run the test with real potential customers

Analyze results and pivot or persevere

Repeat with your next riskiest assumption

This approach minimizes financial risk while maximizing learning speed. You fail fast and cheap instead of slow and expensive.

Principle 5: The Side Hustle Advantage

Some of the world’s most successful companies started as side projects.

Apple began in Steve Jobs’ garage while Wozniak still worked at HP. Craigslist was Craig Newmark’s hobby project while he held a day job. Sara Blakely sold fax machines door-to-door for two years while developing Spanx on nights and weekends.

The side hustle model offers powerful advantages:

Financial runway: Your day job funds your entrepreneurial experiments

Lower pressure: You can take calculated risks without existential anxiety

Validation time: You confirm demand before going all-in

Skill development: You build business capabilities while earning steady income

The key is treating your side hustle with professional seriousness. Dedicate specific hours. Set measurable goals. Track your progress. When revenue consistently replaces your salary or traction proves undeniable, you’ll know it’s time to leap.

Principle 6: The Three Questions That Predict Profitability

Before investing significant time or money in any business idea, filter it through these three questions:

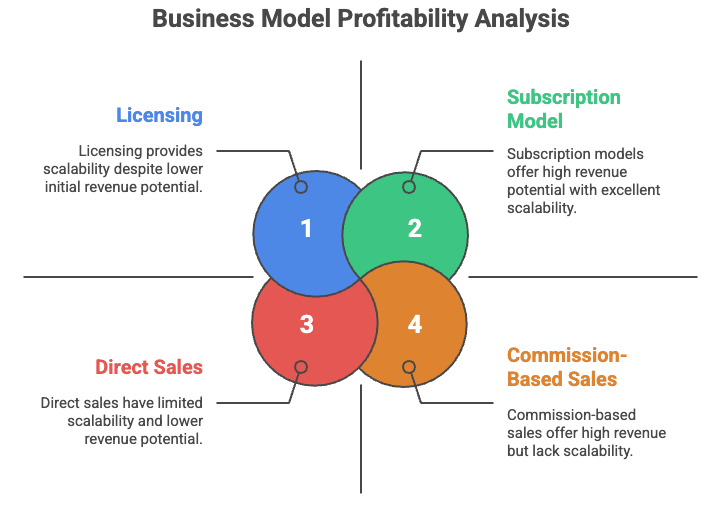

Question 1: How would I get paid with this idea?

This seems obvious, but many entrepreneurs can’t articulate a clear revenue mechanism. Is it direct sales? Subscriptions? Licensing? Advertising? Commission? Know exactly how money flows from customer to your account.

Question 2: How much would I get paid from this idea?

Calculate realistic revenue per customer. Factor in acquisition costs, delivery costs, and your time investment. Many ideas sound exciting until you model the economics and realize you’d need impossible scale to make meaningful money.

Question 3: Is there a way I could get paid more than once?

This question separates linear income from exponential income. Can you create recurring revenue? Can you productize your service? Can one sale generate multiple payment events? The best business models generate revenue that compounds without proportional effort increases.

Principle 7: Forget Demographics, Understand Desires

Traditional marketing teaches you to segment by age, gender, income, and location. That approach misses the point entirely.

What do people really, really want? They want to be happy.

That happiness takes different forms: security, adventure, connection, achievement, freedom, meaning. Your job is understanding which form of happiness your specific customers seek.

Nike’s target market isn’t “18-35 year old athletic males.” It’s “anyone who sees themselves as an athlete and wants to perform at their highest level.” That psychographic definition includes the weekend warrior, the aspiring marathoner, and the professional competitor equally.

To understand your audience deeply:

Talk to them directly (not through surveys or focus groups)

Observe their behavior (what they do matters more than what they say)

Identify their frustrations (problems reveal opportunities)

Map their aspirations (the gap between current and desired state)

When you understand desires at this level, your marketing becomes effortless. You’re not convincing anyone of anything. You’re simply showing them that you have what they already want.

Principle 8: Invitation Marketing: The New Paradigm

Old-school marketing persuades. New marketing invites.

Persuasion tactics create resistance. People sense when they’re being manipulated, and they push back. Invitation tactics create curiosity. People lean in when they feel genuinely welcomed.

The distinction shows up in language:

Persuasion: “You need this product because...”

Invitation: “If you’re someone who values X, you might find this interesting...”

Persuasion: “Limited time offer! Buy now or miss out!”

Invitation: “We made this for people like you. Here’s how to get it when you’re ready.”

Bumble’s entire brand is built on invitation energy. Whitney Wolfe Herd created a platform where women make the first move, fundamentally shifting the dynamic from pursuit to permission. That invitation model attracted 100 million users who wanted a different experience.

Create invitations by:

Leading with value (teach something useful before asking for anything)

Respecting autonomy (let customers choose their own timing)

Building genuine relationships (engage as a human, not a sales machine)

Demonstrating results (show transformation, don’t just claim it)

Watch a masterclass in invitation marketing: Simon Sinek’s “Start With Why” TED Talk, demonstrating exactly how great brands invite rather than persuade.

Principle 9: Your First Sale Changes Everything

At the beginning, your biggest challenge isn’t competition. It’s inertia.

The gap between “I have a business idea” and “I made my first sale” feels enormous. But that first sale transforms everything. It proves your concept has value. It generates momentum. It gives you a customer to learn from. And psychologically, it shifts your identity from “aspiring entrepreneur” to “business owner.”

Tactics to accelerate your first sale:

Pre-sell before building: Offer your product or service before it’s complete. If people pay for a promise, they’ll definitely pay for the delivery.

Tap your existing network: Your first customers are likely people who already know and trust you.

Offer a “founding member” benefit: Create urgency and exclusivity for early adopters.

Make it easy to say yes: Remove every possible friction point from the buying process.

Don’t obsess over perfection. Obsess over that first transaction. Everything else builds from there.

Principle 10: Build the Business Around Your Life

The ultimate entrepreneurial failure isn’t bankruptcy. It’s building a successful business that makes you miserable.

“The business is structured around my life, not the other way around.”

This principle doesn’t mean working less or lacking ambition. It means designing intentionally. What do you want your days to look like? How much travel suits you? What kind of people do you want to work with? What impact matters most to you?

Yvon Chouinard built Patagonia around his passion for climbing and environmental protection. The company’s headquarters is in Ventura, California, near great surf and climbing. Employees are encouraged to take breaks for outdoor activities. The business model supports causes Chouinard cares about. He built his ideal life and wrapped a company around it.

Design your business by starting with these questions:

What does my ideal Tuesday look like?

What activities energize me vs. drain me?

What are my non-negotiable personal priorities?

What kind of growth would actually improve my life?

Your business should be a vehicle for the life you want, not a prison you’ve built for yourself.

The Numbers That Define Your Odds

Understanding startup statistics isn’t about discouragement. It’s about preparation.

The good news buried in the data:

Startups with cofounders are 3x more likely to succeed than solo ventures. Partnership isn’t just nice to have. It’s a statistical advantage.

Property startups have a 55.9% five-year survival rate. Finance and insurance hit 49%. If you’re entering these sectors, the odds favor you.

40% of startups are profitable. Another 30% break even. That means most startups aren’t hemorrhaging money. They’re building sustainable economics.

SaaS startups account for 1 in 5 American unicorns. If you can build recurring revenue software, the upside is extraordinary.

The cautionary patterns:

22% of failed startups lacked a sound marketing strategy. Great products don’t sell themselves. Distribution is as important as creation.

Only 0.05% of startups receive venture capital. Don’t build a business plan that requires VC funding to survive. Most companies never get it.

Over two-thirds of startups never deliver positive returns to investors. Even “successful” fundraises often don’t lead to successful outcomes.

Success Stories That Prove the Principles

Sara Blakely: From $5,000 to Billionaire

Sara Blakely spent two years selling fax machines while developing Spanx prototypes in her apartment. She started with $5,000 and no fashion industry connections. Her breakthrough came from understanding women’s frustrations with existing shapewear and creating a product that solved real problems.

She did her own patent research to save legal fees. She created her own packaging to control costs. She personally pitched Neiman Marcus and convinced them to trial her product. Every principle in this article played out in her journey: minimal investment, passion meeting utility, lean testing, invitation marketing, and relentless focus on value creation.

Spanx has never taken outside investment. Blakely maintained 100% ownership until selling a majority stake in 2021 for a valuation over $1.2 billion.

Whitney Wolfe Herd: Adversity to IPO

After cofounding Tinder and leaving under difficult circumstances, Whitney Wolfe Herd could have retreated. Instead, she identified a fundamental problem with dating apps: women faced harassment and unwanted messages constantly.

Bumble’s “women message first” model wasn’t just a feature. It was a complete reimagining of digital dating dynamics. She built the business around a clear value proposition that resonated deeply with her target audience.

In 2021, Bumble went public with a valuation exceeding $13 billion, making Wolfe Herd the youngest woman to take a company public. She proved that starting from disadvantage, with clarity of purpose and genuine value creation, can lead to extraordinary outcomes.

Elon Musk: First Principles Thinking

Whether you admire him or not, Musk’s approach to entrepreneurship demonstrates key principles at scale.

When experts said electric cars couldn’t compete with combustion engines, Musk applied first principles thinking. Instead of accepting industry assumptions, he broke the problem down to fundamental truths: What are batteries actually made of? What do those materials cost? How can we manufacture them more efficiently?

Tesla began by selling expensive roadsters to wealthy early adopters, using that revenue to fund development of increasingly affordable models. Start small, scale fast. Test assumptions. Iterate based on data. The same principles work at $3,000 or $3 billion.

Watch how first principles thinking drives innovation: Elon Musk’s interview on first principles reasoning breaks down the mental model that’s built multiple revolutionary companies.

Your Four-Step Action Roadmap

Knowledge without action is entertainment. Here’s how to implement these principles starting today:

Step 1: Validate Before You Build (This Week)

Take your business idea and design the smallest possible test to confirm demand. This might be:

A landing page that collects email signups

Direct conversations with 10 potential customers

A pre-sale offer for your product or service

A social media post gauging interest

The goal: Get real market feedback before investing significant time or money.

Step 2: Answer the Three Profitability Questions (Within 48 Hours)

Write detailed answers to:

How exactly would I get paid?

What’s realistic revenue per customer after costs?

How can I get paid more than once per customer?

If you can’t answer these clearly, your idea needs refinement before you proceed.

Step 3: Identify Your First 10 Customers (This Month)

Don’t think about scaling to millions. Think about serving 10 people exceptionally well. Who are they specifically? What do they care about? How will you reach them? What would make them enthusiastic enough to refer others?

Your first 10 customers teach you everything you need to know about the next 100.

Step 4: Design Your Life-First Business Model (Before You Scale)

Before growth consumes your attention, define:

Your ideal daily schedule

Your non-negotiable personal priorities

The type of work that energizes you

The business model that supports all of the above

Build the life you want, then structure your business to sustain it.

The Opportunity Is Now

The statistics don’t lie: 90% of startups fail. But that number isn’t a ceiling. It’s a filter.

It filters out entrepreneurs who skip validation. Who ignore unit economics. Who build for themselves instead of their customers. Who mistake activity for progress.

You have the principles. You have the data. You have examples of founders who started with less than you have and built empires.

The 10% who succeed aren’t luckier or smarter. They’re more intentional. They test before they build. They create genuine value. They understand that constraints breed creativity. They design businesses that enhance their lives instead of consuming them.

Your move.

The future belongs to those who build it. Start with what you have. Solve problems that matter. Test everything. And structure your success around the life you actually want to live.

Great read Ken, and where I have resided for the past 3+ decades.

Building a business is very different from doing the business, and your blueprint breaks that down in a way most founders need to hear. After 30+ years launching products, campaigns, and now building an entire ecosystem with Infortum, I’ve learned those same lessons — usually the hard way.

A few thoughts from my side of the world:

1. Foundation before fuel.

In the infomercial industry, you could never “scale” a campaign until every part of the offer, fulfillment, and customer journey was airtight. If the foundation cracks when you turn the volume up, the whole machine collapses. Your article nailed that.

2. Systems beat heroics.

I’ve been the “quiet voice” behind over 160 product launches. The ones that became category killers weren’t the ones with the flashiest ads, they were the ones with repeatable systems on the backend. A good offer can sell; a good system lets you sleep at night.

3. The offer itself is the first system.

Most founders try to scale before they have a tight offer. A confused offer never scales. Clarity, benefit, proof, that’s the engine.

4. Culture is the multiplier.

Whether it was my old DRTV teams or my current build at Infortum, I’ve learned that culture determines whether the business grows with you or breaks without you. People underestimate this part of the blueprint.

5. Iteration is a survival skill.

In my world, change isn’t an emergency, it’s the job. The best businesses bake the “pivot process” into the foundation instead of reacting only when something fails. Your blueprint is solid. It reminded me that the real goal isn’t just to grow, it’s to build something that doesn’t fall apart when you’re not holding it together with both hands.

Appreciate you putting this out there.