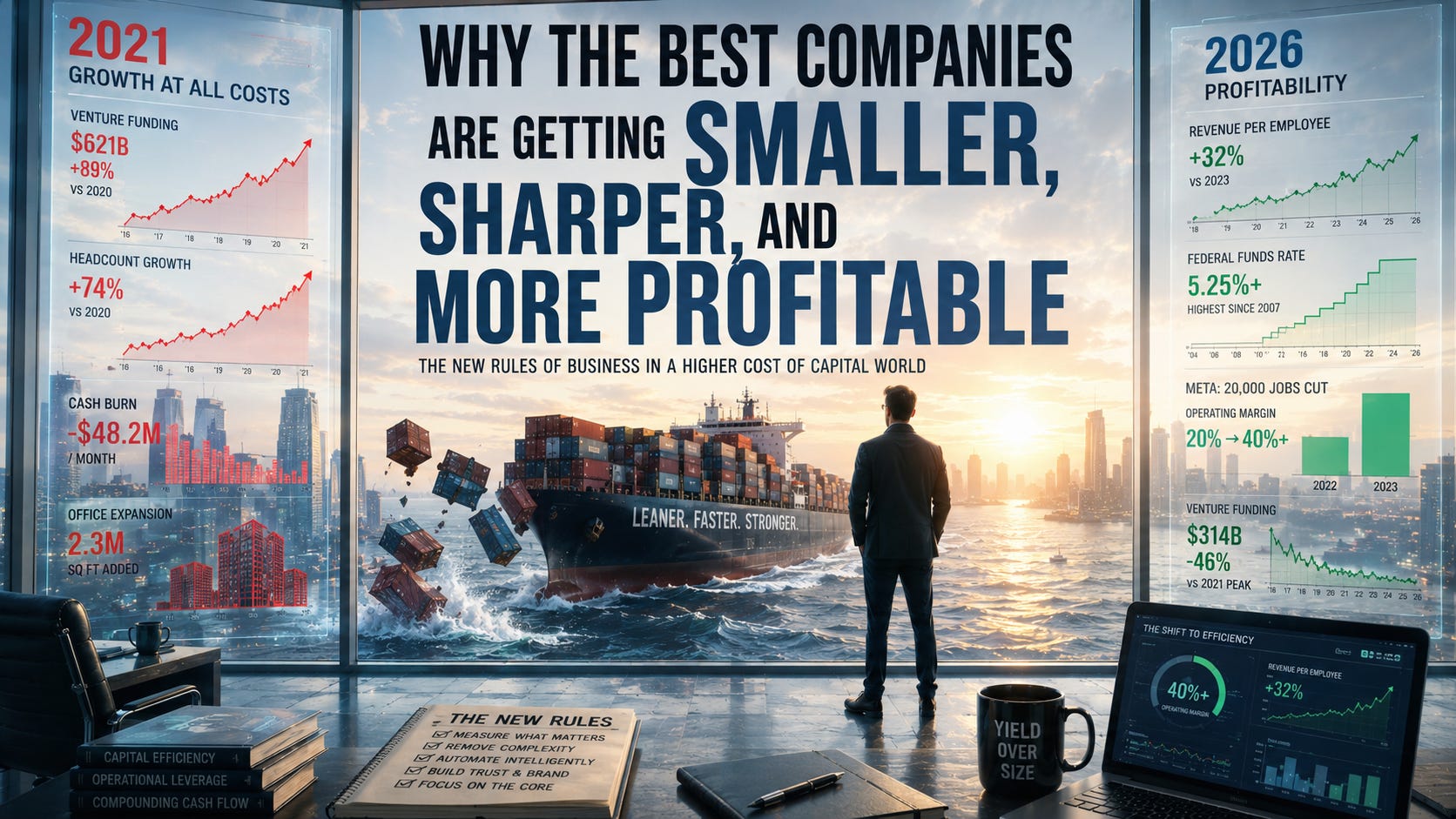

Why the Best Companies Are Getting Smaller, Sharper, and More Profitable

The Day Money Got Expensive Again

In 2021, investors rewarded companies for burning cash. In 2026, they reward companies for printing it.

The change didn’t happen slowly; it hit like a brick wall the moment central bank interest rates crossed 5 percent. Cheap capital didn’t eliminate bad decisions; it simply made them harder to see, making corporate waste look like ambition. The same pitch deck that won applause a few years ago now gets interrupted on slide five with a single question: when does this business produce cash?

For more than a decade, tech and startup culture operated under a dangerously simple assumption: if revenue grew fast enough, every flaw could be ignored. Profitability could wait. Operational discipline could wait. Efficiency could wait.

The single objective was scale. Founders raised massive rounds, hired sprawling teams, leased expensive offices, and justified deep losses in pursuit of future market dominance. For a long time, investors rewarded them for it.

That environment no longer exists. Money became expensive again. Top-line expansion is no longer evaluated in a vacuum; the margin profile of that revenue has become one of the central tests of corporate health.

Capital efficiency is not about spending less. It is about converting each dollar into more learning, more revenue, and more durability. McKinsey’s value-creation research has repeatedly found that companies combining strong growth with profitable growth outperform those chasing growth without durable returns. Growth still matters, but cash flow carries equal weight.

The leaders creating the most resilient businesses today are not the ones raising the largest financing rounds. They are the operators building highly productive, agile structures that generate more output, more cash, and more choices with fewer resources.

The critical question for the modern boardroom has shifted: it is no longer just how rapidly a company can expand but how efficiently it can do it.

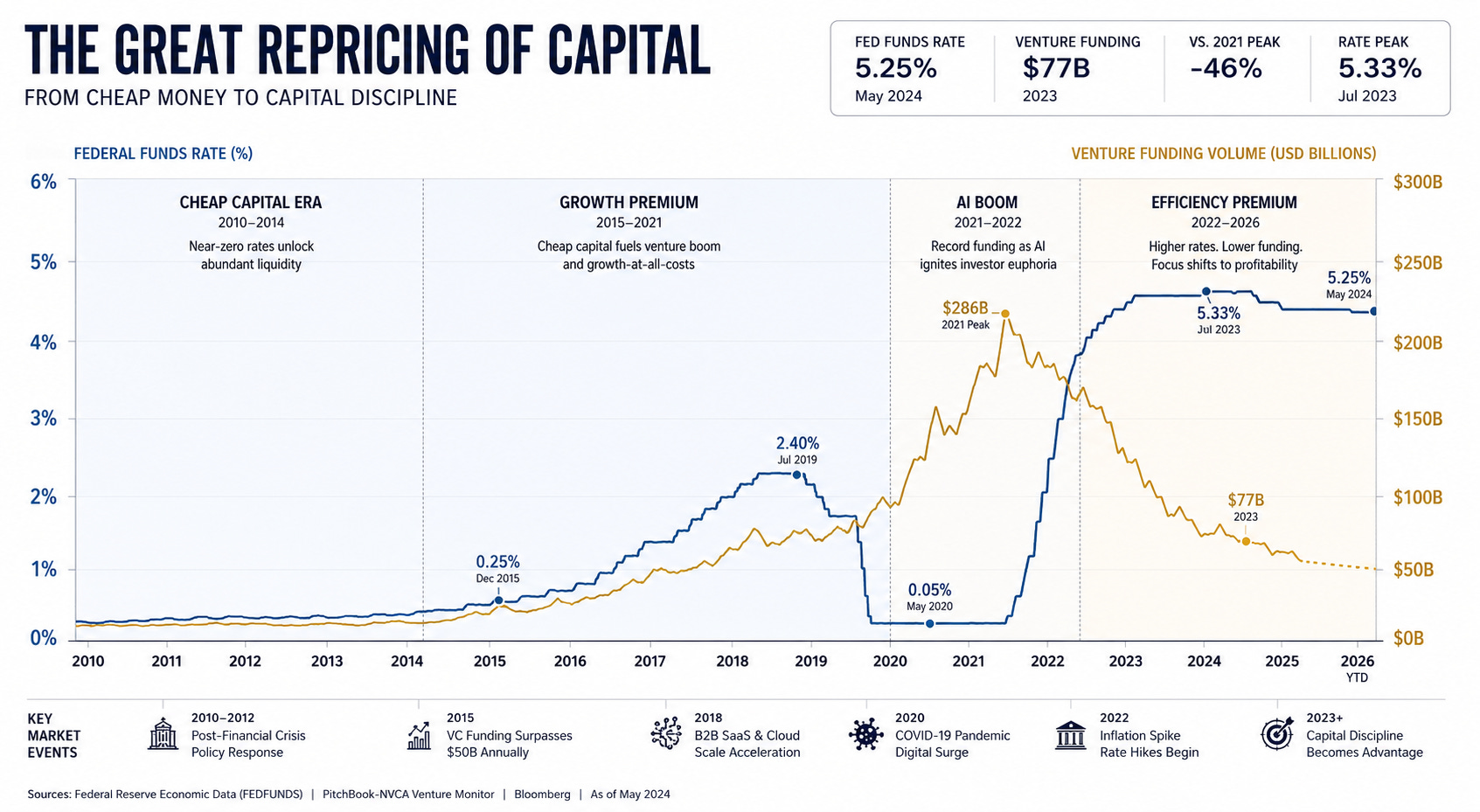

The Great Repricing

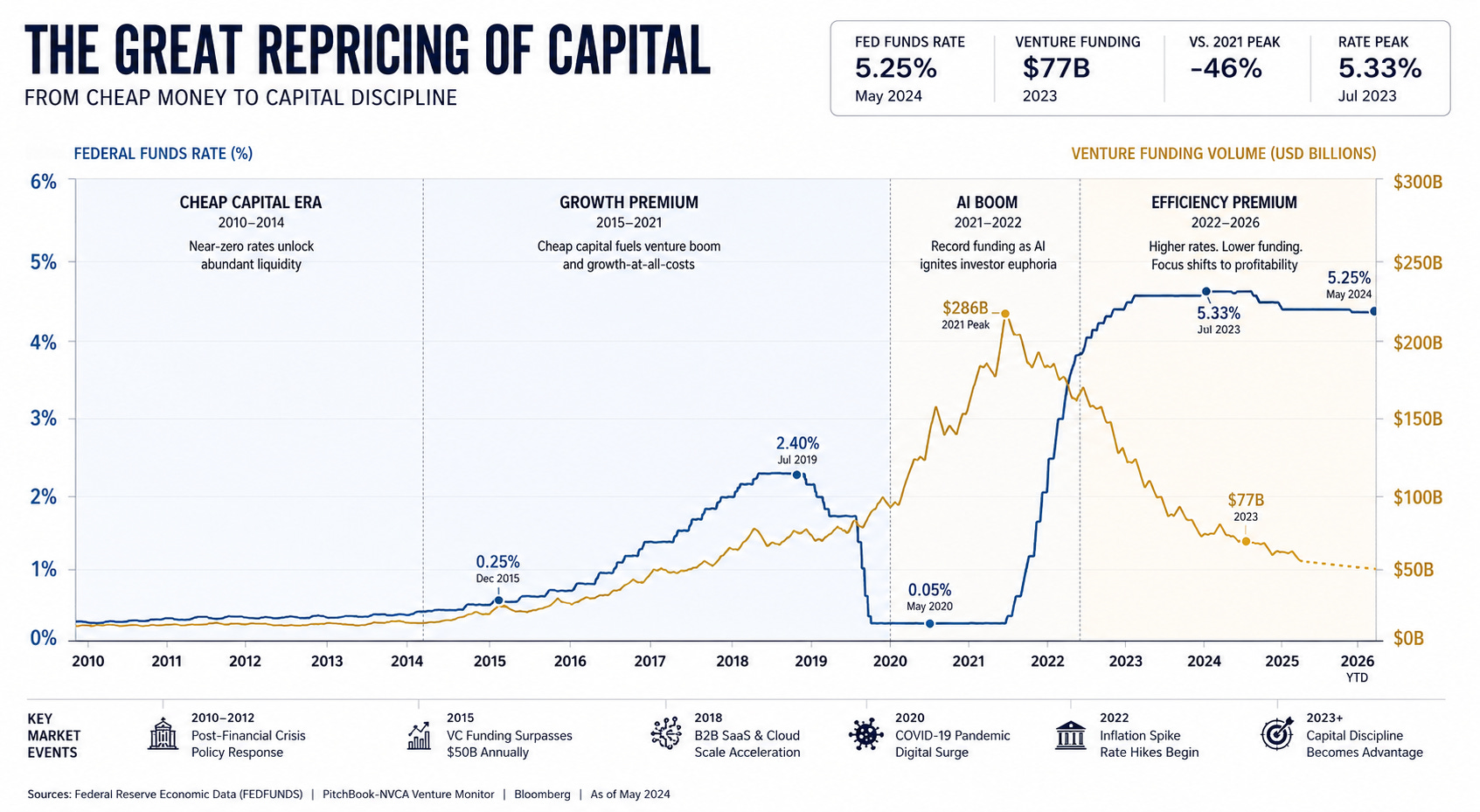

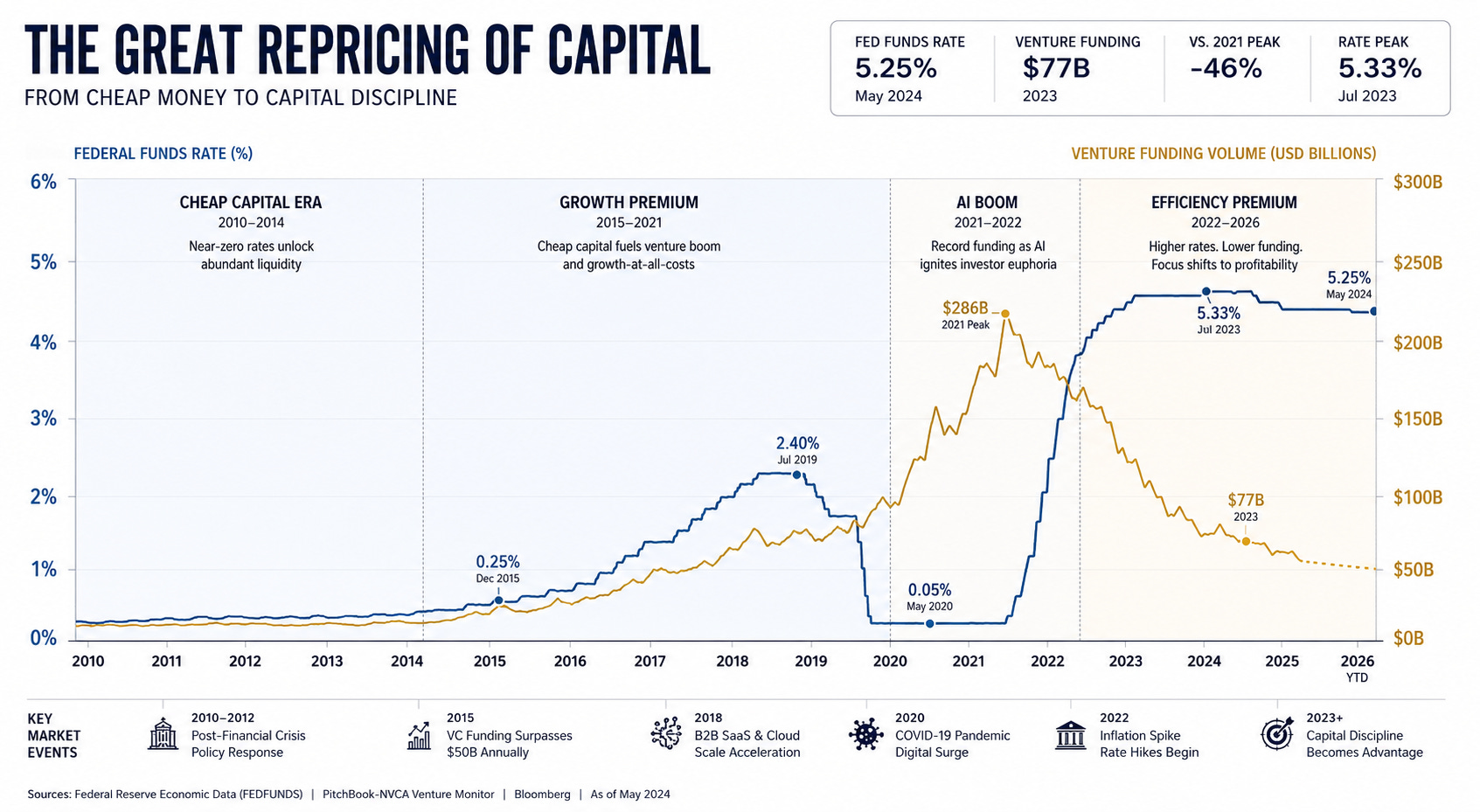

To understand how we arrived here, we have to look at the economic shift that re-indexed the entire business world. Between 2010 and 2021, near-zero interest rates created a historic abundance of cheap capital. With nowhere else to find yields, institutional money flooded into venture capital and private equity.

Because capital was plentiful and cheap, investors optimized for the highest possible future valuation. They paid a growth premium, essentially telling founders to burn through cash as fast as possible to capture the market, leaving margins for later.

Then the macroeconomic environment changed. According to Federal Reserve rate data, central banks raised the federal funds rate from near zero to over 5 percent to combat inflation. As a consequence, private capital markets tightened, venture funding dropped sharply from its 2021 peak, and public SaaS valuation multiples compressed.

The growth premium vanished, replaced by an efficiency premium. Investors stopped asking how fast you could grow and started asking when the business would produce cash. This wasn’t just a minor market correction; it was a fundamental repricing of risk, leverage, and corporate value. Founders who failed to adapt to this shifting financial landscape quickly found their runways cut short.

Why Startups Should Focus on Profitability | Y Combinator

The shift from growth-at-all-costs toward sustainable businesses reinforces the macroeconomic repricing.

The Headcount Illusion: Complexity vs. Actual Scale

One of the most persistent misconceptions in management is the belief that a larger team automatically creates a stronger company. In practice, adding personnel ahead of clear operational necessity introduces exponential complexity. Communication pathways multiply, decision cycles lengthen, and coordination costs surge. Managers spend more time aligning internal teams and less time shipping products.

For years, growing a workforce was a public status symbol. Hiring surges generated headlines, and massive offices projected commercial momentum. Then reality arrived. Following the venture funding contraction, the tech sector witnessed a wave of structural corrections, with data from the Layoffs.fyi tech layoff tracker is counting hundreds of thousands of startup layoffs globally since 2022.

The corporate response from category leaders demonstrated that leaner teams could yield superior outcomes. Meta Platforms Inc. became the anchor case study for this shift when it cut more than 20,000 jobs across its 2023 “Year of Efficiency” restructuring. Rather than triggering a collapse, the cuts forced a company-wide reassessment of management layers, decision speed, and operating discipline.

The result, detailed in Meta’s 2023 annual report, was an immediate operating margin recovery from 20% in late 2022 to over 40% by late 2023, paired with a historic stock price rebound. Zuckerberg championed a “flatter is faster” argument, noting that a leaner organization performed better because it empowered individual contributors and removed unnecessary layers of approval.

A parallel lesson emerged at X (formerly Twitter). Following its ownership transition, the company executed workforce reductions of approximately 80 percent. X is not a clean model to copy; it is a stress test that exposed how much excess capacity large platforms can carry. While the platform faced significant advertiser loss, reputational damage, and operational controversy, the core technology architecture continued to function, defying predictions of an imminent systemic blackout.

Shopify’s workforce reset and renewed focus on core commerce infrastructure offer a cleaner example of the same pattern. Shopify’s reset became a useful example of a company narrowing its focus after a period of overexpansion, emerging with sharper focus and a highly optimized product baseline.

Ultimately, headcount is a misleading metric for scale. True scale is defined by leverage. The highest-performing firms evaluate success based on a simple baseline metric: annual revenue divided by average full-time-equivalent (FTE) headcount. They build their cultures around a fundamental operating question: How much value can a small, highly aligned team create?

Mark Zuckerberg on the Year of Efficiency

Why AI Does Not Fix Broken Workflows

With efficiency dominating the corporate agenda, many leadership teams have turned to artificial intelligence as a universal remedy for waste. Yet, a substantial portion of enterprise AI initiatives fail to deliver measurable productivity gains. The underlying issue is usually the structural design of the workflow, not the technology’s capability.

A poorly designed process does not become efficient simply because an AI tool is integrated into it. A support organization with five approval layers doesn’t become efficient because it buys AI. It becomes efficient when it removes three approvals. Applying automation to a broken, convoluted workflow merely accelerates waste.

Industry tracking from Gartner’s research on emerging technology indicators points to a widening performance gap between organizations that merely deploy generic AI copilots for individual task automation and those that completely redesign core business workflows around task-specific AI agents. As autonomous execution models mature, the focus is shifting away from simple text completion toward platforms featuring embedded, independent agents capable of automated execution.

The companies extracting the highest returns from automation take an inverse approach. They begin by evaluating the workflow from first principles, entirely independent of software. They eliminate redundant approvals, remove manual data handoffs between disconnected systems, and simplify the operational sequence. Only after the workflow has been stripped of unnecessary complexity do they introduce automation layers.

The objective of an AI integration should not be to create a marginally faster iteration of an outdated process. The objective is to establish an entirely different operating model. In a properly optimized architecture, human staff stop functioning as manual data routers. Their responsibilities shift toward strategic judgment, creative execution, exception handling, and high-stakes decision-making, while the underlying technology framework handles the automated execution.

Brand Is a Margin Strategy

Once a company has disciplined its internal machine and streamlined its workflows, the next critical question is whether the market understands why that machine deserves premium economics. As customer acquisition costs (CAC) continue to escalate across traditional digital marketing channels due to increased ad-auction competition and shifting privacy frameworks, building a distinct brand ceases to be a purely creative endeavor. It becomes a critical operational asset.

Building Products People Love

Many founders still treat branding as a decorative exercise, spending excessive executive cycles debating logos, typography, and color palettes while ignoring the quantifiable economic utility of brand equity. A well-defined, highly credible brand reduces market friction throughout the entire customer lifecycle.

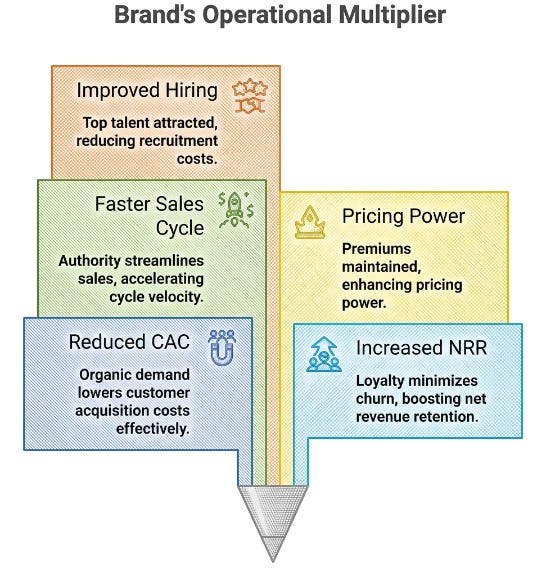

When properly executed, a strong brand acts as an operational multiplier across several key business metrics:

Customer Acquisition Cost (CAC): Drives organic inbound demand, potentially reducing dependence on paid acquisition.

Net Revenue Retention (NRR): Fosters long-term loyalty, insulating the business from competitor churn tactics.

Sales Cycle Velocity: Minimizes the friction of prospect education, establishing authority before the initial sales conversation begins.

Pricing Power: Grants the enterprise margin defense, allowing the company to command premiums even during broader economic contractions.

Hiring Quality: Attracts top-tier talent organically, reducing expenditures on recruitment and headhunting fees.

This mechanism is highly apparent in the B2B software sector with a company like Linear. In a crowded market of project management software, Linear shows how a sharp product narrative can create unusually strong loyalty among engineers. That loyalty can reduce dependence on paid acquisition and give the company more pricing flexibility.

This deep trust fundamentally changes consumer purchasing behavior. When buyers perceive competing market options as functionally interchangeable commodities, price inevitably becomes the deciding factor, sparking a race to the bottom that erodes margins. Conversely, when a customer base perceives deep credibility and identity alignment, price sensitivity diminishes. In highly saturated markets, a well-entrenched brand represents a defensible operational shield for corporate margins.

The Discipline of Spending Well

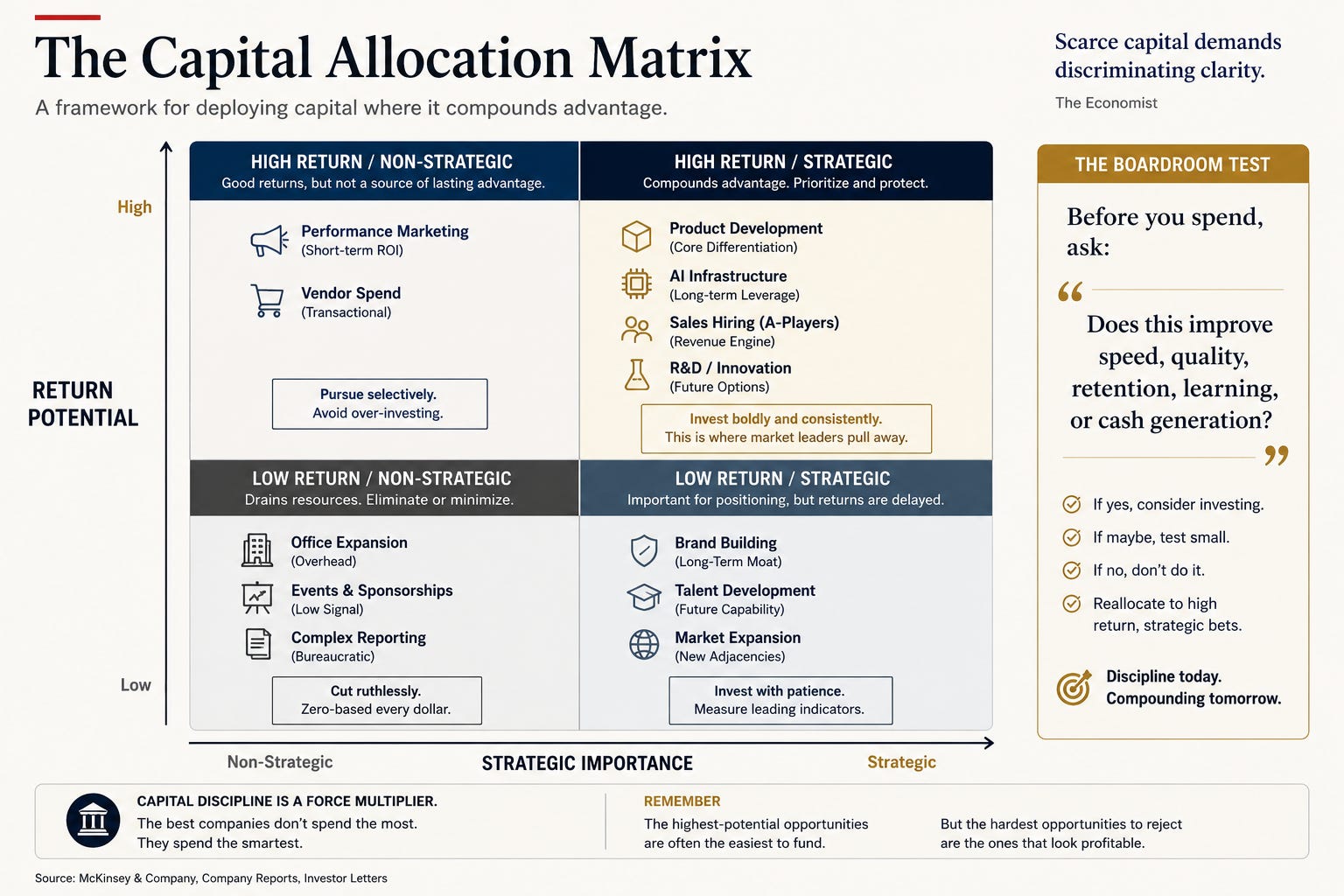

Adopting a capital-efficient operational model does not require a leadership team to embrace fear-based austerity, nor does it mean starving the organization of growth capital or avoiding high-stakes strategic investments. Capital efficiency is not spending less; it is getting more learning, more revenue, and more durability from every dollar spent.

True financial discipline means deploying capital with absolute intention, ensuring that every dollar allocated has a clear strategic purpose, a defined hurdle rate, and a measurable return. Founders can run their choices through a simple boardroom test: If a dollar does not improve speed, quality, retention, learning, or cash generation, it deserves immediate scrutiny.

This principle is universally applicable, whether a company is bootstrapped, debt-financed, or venture-backed. Institutional venture capital is not inherently problematic; indeed, many capital-intensive industries require massive, concentrated upfront investment long before achieving self-sustaining cash flows. Deep-tech sectors like semiconductor manufacturing, artificial intelligence infrastructure, biotechnology, aerospace, and advanced energy systems cannot scale without significant injections of external primary capital.

The structural danger emerges when management uses external funding rounds to mask broken underlying business fundamentals. No volume of venture capital or venture debt can permanently compensate for structurally negative unit economics or a fundamentally unviable customer acquisition model. Eventually, the market adjusts, the capital subsidy ends, and the business faces severe distress.

The most sophisticated operators construct internal systems capable of proving cash-generation viability at a micro-scale before seeking funding. They treat external capital as an accelerator for a working engine, rather than a fuel source to keep a broken engine running. This distinction separates an enduring commercial enterprise from a runway experiment.

Focus as a Competitive Moat

Companies rarely fail due to a total starvation of commercial opportunities. More frequently, they decline because they attempt to pursue too many opportunities simultaneously, diluting their operational focus.

Initial commercial success invariably introduces new forms of corporate risk. As a core product gains market traction, customers begin requesting adjacent features, secondary markets appear highly lucrative, and strategic partnership opportunities multiply. The temptation for the founding team is to expand the scope in multiple directions at once, chasing incremental revenue streams at the expense of core execution. The hardest opportunities to reject are the ones that look profitable.

When resources are distributed across too many disparate initiatives, organizational momentum fragments, complexity climbs, and executive execution suffers. The companies that maintain elite market positioning over long horizons display a contrarian characteristic: a willingness to decline attractive but non-essential distractions.

These organizations recognize that true strategic focus is not merely identifying a primary path to pursue; it is the deliberate discipline of identifying what not to do. Every category-defining company eventually faces this inflection point. The operators who build lasting legacy businesses become known for doing a few things at an elite standard, while struggling organizations frequently fade by trying to accommodate every market whim.

Where Capital Efficiency Can Go Too Far

An objective analysis of capital efficiency requires recognizing its structural limits. When efficiency transitions from a data-driven operational strategy into a dogmatic system of fear-based austerity, it can actively jeopardize the long-term viability of the company.

Customer Experience Degradation: Chronic under-hiring within client services, account management, or technical support operations frequently leads to increased response times, lower customer satisfaction scores, and eventual revenue churn that offsets short-term payroll savings.

The Deep-Tech Capital Imperative: Categories such as biotechnology, quantum computing, aerospace, and semiconductor fabrication cannot operate under hyper-lean, near-term cash-flow mandates. These sectors require prolonged periods of heavy, upfront research and development capital before producing commercial yields.

Innovation Starvation: If an organization cuts all expenditure that does not yield an immediate, identical-quarter return, it effectively eliminates its ability to engage in horizon-three R&D. Over time, this leaves the core business highly vulnerable to sudden technological shifts.

Efficiency should never be used as a euphemism for corporate starvation. The objective is optimization, ensuring the organization has the financial resilience to fund its most critical choices.

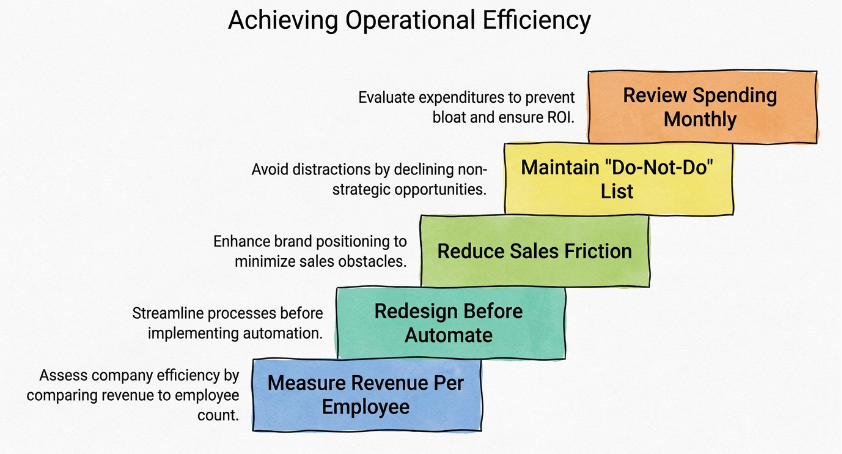

Five Operating Rules

Measure Revenue Per Employee If the number isn’t improving, the company isn’t becoming more efficient. Benchmark your annual revenue divided by average full-time-equivalent (FTE) headcount against the top decile of your specific industry vertical.

Redesign Before You Automate Never automate waste. Map every operational touchpoint of your most time-consuming process and eliminate duplicate data entry or redundant approvals before writing a single line of software code.

Make Your Brand Reduce Sales Friction Refine your positioning to focus explicitly on category expertise and your unique operational worldview to eliminate product-specification comparison and build immediate margin defense.

Keep a Formal “Do-Not-Do” List Author a formal operating document that details the products, features, and client profiles the company will deliberately decline to pursue. This serves as your primary shield against shiny object syndrome.

Review Spending Choices Monthly Review corporate capital deployment, vendor expenditures, and return metrics with your executive team every 30 days. Evaluate every subscription, retainer, and marketing channel against the boardroom test filter to prevent bloat.

The next generation of great companies will not win because they hired the most people or raised the most money. They will win because they learned how to create more value with less.

Size used to be the signal. Now the signal is yield.